Your Auto Insurance rates are rising, and you are wondering why…

There are a number of factors that most insurance providers use to calculate how much you’ll end up paying for your auto insurance. The coverages you choose, where you live, the kind of car you drive, how your car is used, who drives the car, and information from consumer reports impact the cost of your car insurance. Many of these factors are out of your control, but not all of them. This list can be used as a reference to help lower your costs, while protecting what’s important to you.

- Your Coverage and Deductibles

Car insurance providers allow you to choose your deductible and decide whether to add additional coverage that isn’t necessarily required by the laws in your state. The specifics of your coverage and deductibles play a major role in your monthly payment.

A car insurance deductible is the amount of money you have to pay toward repairs before your insurance covers the rest.. For example, if you’re in an accident that causes $3,000 worth of damage to your car and your deductible is $500, you will only have to pay $500 toward the repair.

Typically, choosing a higher deductible means a lower monthly payment; choosing a lower deductible means a higher monthly payment. Additional coverage gives you added financial protection, depending on the claim, but will also add to your monthly costs.

2. The Type of Car You Drive

One of the factors that you can control is the kind of car you drive. The safer the vehicle is, the lower the cost will be. A vehicle that is full of safety features such as air bags, seat belts, anti-lock breaks, and traction control will actually lower your cost. Reports have also shown that the larger the vehicle is the less likely it is to be involved in accidents.

On the other hand, having a car that can reach high speeds, is loaded with new technology, and is smaller in size can make the vehicle and passenger have a higher rate of accident and injury. It can also create a more expensive cost to repair damage, while increasing the chance of theft. These kind of vehicles will likely increase the cost of your rate.

Next time you head to the dealership, keep these factors in mind when choosing your new vehicle. There are many options these days, so there are still ways for the car enthusiast to find a happy medium.

3. How Often, And How Far, You Drive

If you are using your car for business, and long distance commuting, you typically pay more than those who drive less. The more miles you drive in a year, the higher the chances of an accident – regardless of how safe a driver you are.

To lower your rates consider car pooling, riding a bike, or taking public transportation to work. By reducing your total annual mileage, you may be able to reduce your premiums.

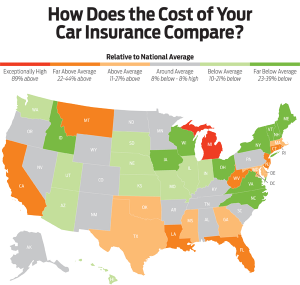

4. Where You Live

Where you live matters. Your location affects Auto Insurance Rates

In Urban Areas driver typically pay more for their insurance due to a higher rate of vandalism, theft, and accidents. On the opposite side, if you’re living in a rural community with a lower population density you will have a better chance at decreasing your rates. For a rule of thumb: The more people that live in your area, the higher your rate will usually be.

5. Your Driving Record

Have you been in a lot of accidents? Have you gathered a nice collection of speeding tickets? Then the chances are your rates will be higher than someone who hasn’t. Although your driving record can’t be erased, over time you can prove to insurance companies that you have left your reckless driving habits in the past, which will eventually decrease your out-of-pocket cost.

6. Your Credit Score

Many insurance companies use credit score to predict future insurance claims. While there is no definite point at which your credit score begins to affect your rate, generally lower scores means higher insurance premiums. Make sure you know your credit score, and do what you can to improve them before purchasing auto insurance.

7. Your Age, Sex, and Marital Status

Young male drivers are statistically at a higher risk than young female drivers to get into an automobile accident. Still, young drivers under the age of 25, regardless of gender, are going to pay higher premiums. This is because younger drivers statistically drive more recklessly, get in more devastating accidents, and drive with more distractions. They are also not as experienced. Teen drivers can still receive discounts on auto insurance by completing programs like drivers-ed.

Married people tend to have fewer accidents than single people; therefore, getting married (especially for men) can significantly lower your rate. How much your rate decreases depends on your previous driving history – if you are a man who has never been in an accident and has a clean driving record, you could see your rates drop quickly.

Overview:

Not everything is in your control regarding your auto insurance rates, but for the factors that are, there are a few simple steps you can take to lower your premiums.

Choose the right car and location to live for where you are in your life. Drive safely and follow the law of the road, stay out of debt to the best of your ability, and educate your youth on how to properly handle the road. By taking these steps you will increase your likelihood of lowering your auto insurance rates.

For more, follow us on Facebook, and Twitter.

You can also sign up for our insurance newsletter by following the link below:

Bisnett Insurance is a proud independent insurance agency located near you. We have been providing our customers with trusted insurance advice for over 35 years throughout Oregon, Idaho, and Arizona. We are professionals here to provide you with peace of mind.

Follow Us!